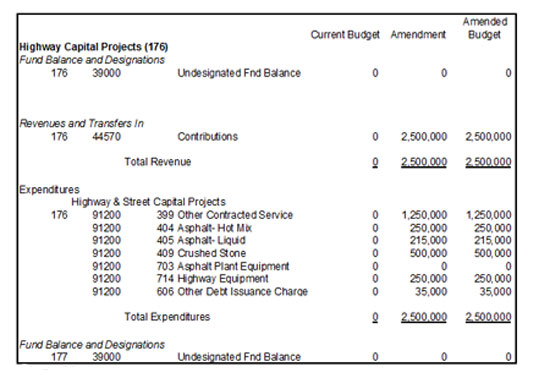

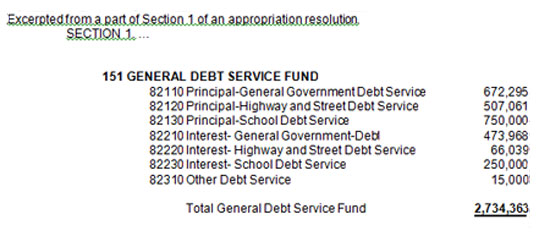

The comptroller’s office accepts the bond or note approval by the county commission as authorization to establish an appropriations budget. It is highly recommended that an official budget be established reflecting the receiving of the borrowed funds along with the expenditure budget. This receipt and expenditure budget would be in either a Capital Project Fund or an Operating Budget. Figure 10 reflects a sample budget being established for the receipts and expenditures of a Highway Capital Project Fund. The annual expenditures of interest and principal are required to be annually appropriated. This appropriation should be reflected in the appropriations resolution and broken down by the respective classification in which the funds were borrowed. Figure 11 reflects an excerpt from an appropriation resolution.

Recommended Practice: An official capital budget should be established and filed with the county legislative body before or after the issuance of debt.

Recommended Practice: A budget amendment may be needed if new indebtedness causes the payment of interest and/or principal in the year of issuance.

Figure 10

Figure 10

Figure 11

Figure 11