Reference Number: CTAS-1759

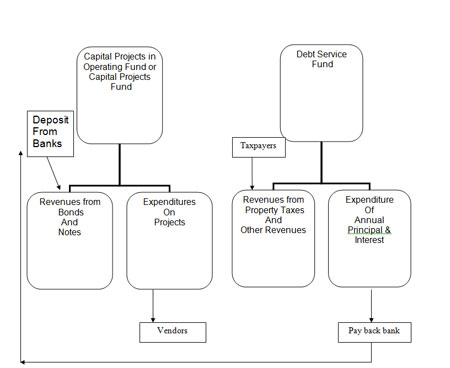

Figure 4 shows the Debt Service Accounting relationship. Figure 5 shows the Flow of Money relationship. In summary, monies are borrowed from banks and financial institutions and receipted into an operating fund (other than debt service) or capital fund(s). These operating funds or capital funds are used to purchase the asset(s). The indebtedness due to the borrowed monies is then paid annually by the retiring of this debt by way of the annual debt service operating budget.

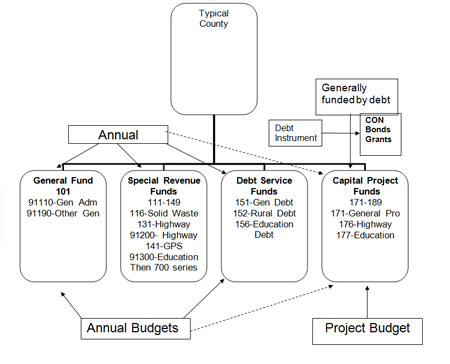

Figure 4

Figure 4

Flow of Money-The Debt Service Fund

Figure 5

Figure 5