We would be negligent if we did not discuss the matching principle of accounting as it relates to the annual operation of the local government. An easy way to describe this principle is the philosophy that an asset should be paid for during the time the asset is in use. This principle has some weakness, but a straight forward example of this matching is as follows: A government purchases land and constructs a library building at the cost of $1 million. The land has an infinite life expectancy, but the building, properly maintained, may be used for 30 years. Should the taxpayers who have access to the use of the building 30 years from today pay a portion of the cost? If you answer yes, then this is a belief in the matching principle. In the new approach to making government accounting look more like commercial accounting, we now use depreciation to reflect this cost. However, depreciation is not a cash accounting entry; but if debt is issued, the payment of principal and interest is a cash payment and therefore a 30-year bond payment schedule reflects what is paid by current and future taxpayers throughout the useful life of the loan, thus the use of the building.

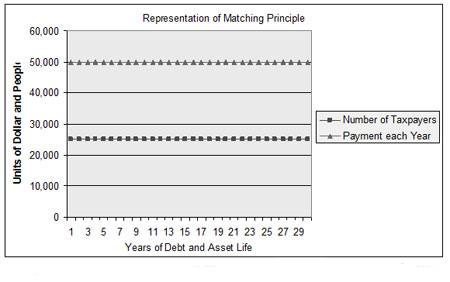

Now the matching principle as it relates to payment of debt is never exact with the asset’s useful life, but it can fairly represent matching use of the asset with payment for the use of the asset. Some weakness in pure matching deals with time value of money; useful life exceeding or being less than planned debt or planned life; and more or fewer taxpayers making debt payments or using the asset over time along with issues of changes in value of property. Figure 1 reflects a pure relationship with a set number of taxpayers.

Figure 1

Figure 1

Figure 1 reflects that each taxpayer pays $2 per year for the assets use for 30 years.